A Potential Fed Put

Actionable Market Insights from Tuttle Ventures

Welcome to the +21 new subscribers this week and +287 over the last 90 days!

If this is your first time, we share actionable market insights and portfolio updates so YOU can make better investment decisions and get an inside view at Tuttle Ventures.

I highly encourage newcomers to go back and read through our past 50 newsletters since we started writing 1 year and 2 months ago—

Packed with:

Macro Views: Our Landmark Inflation Call, Why Bond Math Didn’t Look Good

Portfolio Positioning: The Short Answer for our Short, 2021 Recap

Private Investments: Boxabl, Socket Security, Midtown National Group (MNG)

Key Business Highlights: Forbes Article, Awards, & TV Appearances

Why I Advise other Investment Advisors: Who Advises your Advisor?

All available — in the archive —at no cost.

Ok, now back to our regular scheduled programming.

This week has been busy—we are in full swing for Advisor Investment Committee’s, earnings season and the market has been flirting with a potential Fed pivot.

I’ll be brief:

Our Quote in U.S. News & World Report

A Potential Fed Put

Portfolio Updates

Final Word

Our Quote in U.S. News & World Report

Our research was quoted in U.S. News & World Report!

The article is titled:

“How to Invest In Lithium Stocks as EV Demand Grows”

This research was done to evaluate the Lithium industry. I shared our key takeaways on Twitter and a reporter reached out if I would be willing to go on record.

The lithium industry fuels the electric vehicle industry, which explains the high demand for the metal.

We consider the AISC (All in Sustaining Cost) a must have metric for any mining investment. It’s our goal to coach you through responsibly so you don’t have to painfully learn what we already know.

You must carefully consider the costs of extraction for mining investments.

At Tuttle Ventures, we pride ourselves on being proactive rather than reactive to an ever changing investment landscape.

We will continue to provide unique ideas backed by interesting research so you can reach your financial goals.

A potential Fed Put is Brewing

The term "Fed put," a play on the option term "put," is the market belief that the Fed would step in and implement policies to limit the stock market's decline beyond a certain threshold.

Let’s quickly look at the National Financial Conditions Index.

If you need a recap of this metric and why we use it, go back to last week’s newsletter 3 Strikes to Signal a Recession.

All you need to remember is Positive values of the NFCI have been historically associated with tighter-than-average financial conditions.

Negative values have been historically associated with looser-than-average financial conditions.

In the chart above, you can clearly see that conditions have shifted, turning negative, indicating we are back to looser-than-average financial conditions.

This means financial conditions last week were *not* getting tighter.

We are not sure, but this may potentially indicate a turning point.

If you break down the numbers from Risk, Credit, Leverage, & Adjustments; the biggest swing came in financial engineering from the “Risk Category”.

Institutional investors took on more risk last week. You can access the full list of indicators here.

Remember, we expect a recession, with a lag, after monetary policy gets tighter.

But what if the Fed is already starting to ease?

What if the *signal* of Quantitative Tightening (QT) to the market was enough to get the "peak inflation" narrative under control.

Institutional Investors are acting as if that was true, buying up stocks, and taking on more risk.

That would mean a potential “Fed Put” is back on the menu- the Fed accomplished the goal of curbing inflation and now could go back to easy money.

This would be bullish for stocks and bonds.

We are waiting on two things before we turn bullish for stocks and bonds:

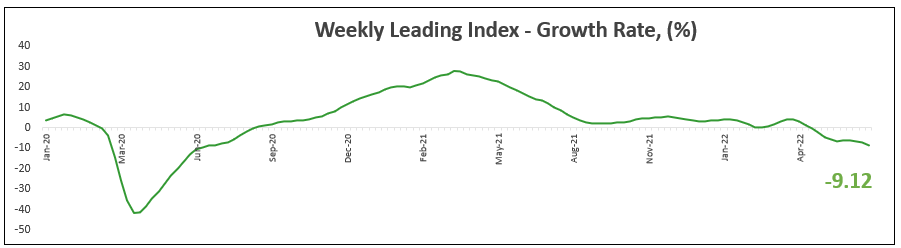

We need the ECRI US Weekly Leading Index to confirm that the economy has turned upward and is positive.

We need the S&P 500 index to break above its 50-week simple moving average.

It should be noted that weekly moving averages are very different from daily moving averages that most investors are used to.

This may mean we don’t catch the exact bottom when as it happens but we are ok to wait for a clear signal.

Now that Michael Barr has been voted in, the Fed just got a new voting member on team easy money.

Quantitative Tightening (QT), at least as the Fed is implementing it—is not the opposite of Quantitative Easy (QE), because it is shrinking the balance sheet by stopping reinvestment of matured (or prepaid) securities rather than selling assets.

The extent of duration being put back into the market could be far lower than what the roughly $2.5tn reduction in size suggests.

This is especially the case when it comes to USTs. The Treasury is likely to replace a sizable portion of lost Fed financing by bill issuance, which would not represent a material change in duration supply.

This is essentially the shell game of a new Fed Put.

Instead of really tightening conditions- they flood the market with Treasury Bills equal to the size of matured securities, really never tightening at all.

Funding long term liabilities with more short term debt.

At least, that is what I think the latest scheme is from the Fed, based on what was published this week out of Atlanta:

“Quantifying "Quantitative Tightening" (QT): How Many Rate Hikes Is QT Equivalent To?”

The Fed is trying to have its cake and eat it too.

They plan to hike rates without a recession by pushing short term treasury bills to fund easy money.

As of for now, it looks like it has bought them time.

Portfolio Updates

This week we made one trade. Let me explain: