The Short Answer for our Short

Vision | Courage | Patience for Successful investing with Tuttle Ventures

*Welcome to the 33 new subscribers who joined this week*

We promise to show up every week to give you actionable market insights.

You get an inside view into Tuttle Ventures with portfolio updates so you can make smarter investment decisions.

Learn. Build. Share. Grow.

Newsletter rundown:

Trades this week

Why we are going net short

The Biggest Influence on me as an Investor

My best podcast yet

Housekeeping

There’s a lot to unpack so I’ll just jump right into it.

Courage

We are going to be humble when we say that The Fundamental Value Portfolio has caught the regime turn (that folks have predicting for *years*) from falling to rising rates, from monetary to fiscal policy dominance, from deflationary to inflationary, growth to value, from passive to active. With trades to back it up.

Part of this was due in part to starting Tuttle Ventures at a time that allowed us to have *clean slate* allocations with plenty of cash.

Another was luck

A third was a new found courage to invest “outside the social narrative” which was influenced by the fallout and lost faith in institutions post-covid.

No one knows for certain what’s going to happen in the future, but we believe successful investing takes, Vision, Courage and Patience.

This next week we will apply Courage.

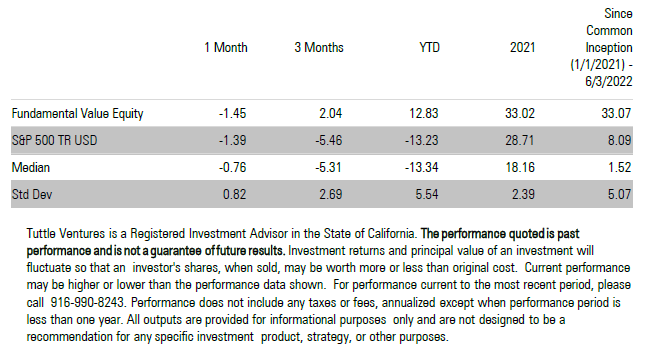

TV’s core portfolio holdings and performance as of 6/5/2022:

Our May 2022 Fund Factsheet and Investment Performance is now live.

Sold last Week and Increased Cash

This week we sold two holdings at a net gain to cash.

First, we sold 50% of our existing position in $OLN at our price target of $65, so it is now a 5% holding (similar to Mosaic $MOS). Our rationale for the sale can be read in last weeks newsletter here.

We also sold out of $CPB, Campbell Soup Company at $48. The purpose of this sale is less about the individual company outlook and more about overall portfolio positioning based on our macroeconomic view.

We see the urgency to decrease our Portfolio Beta from 0.50 to 0.25

We believe the US future mirrors Japan’s Lost Decade of the 90’s.

Selling Campbell gets the portfolio back into our beta range. Campbell also had the least upside potential of all of our current holdings.

We had been using the consumer defensive sector and Campbell’s inferior good quality (demand increases even when incomes decrease) as a defensive prop.

Another reason for the sale is that Campbell had a higher “bear beta” than we would like vs. a net short position.

The purpose of the sale was to:

decrease our overall sensitivity to the market

create cash so we can establish a net short position next week.

Why we are adding a net short this week

We are adding a net short because:

We believe the equity market has further to fall

We anticipate a net short is less risky than a new net long

We will keep strict risk controls in place so we can adapt as needed

That’s the short answer for our short.

The biggest influence on me as an Investor

George Friedman has had the biggest influence on me as an investor.

I first read The Next 100 Years back in 2010, when I was living in Ethiopia as 21-year old missionary.

If I was in the War Room and could only bring one other person, George would get my call. I read everything he writes.

George’s unmatched analysis in geopolitics has led him to regularly brief military organizations and consult for Fortune 100 executives.

History doesn't repeat itself, but it often rhymes

The privilege that people like George have to opine on Geopolitics and Geoeconomics is only because the US has risen to a position of power and prosperity.

Over the last 40 years, a billionaire class and corporate monopolies with deep pockets had big ambitions for global supply chains and coordinated policymaking for the “greater good”

According to George Friedman, for the first time in a long time, both the Institutional and Socio-Economic cycles will be culminating within a few years of each other.

This is not positive for risk markets.

To quote George Friedman:

“War planners must plan on capabilities, which are much slower to change than intentions.”

The Federal Reserve quantitative tightening creates the capability of a market downturn, even if it is not their intention.

My Best Podcast Yet

I summarized some of these thoughts in a conversation with Anthony Fatseas. This is a repeat from 11 months ago when we talked about market influences and you can listen more here:

1:30 - Current Macroeconomic trends?

6:45 - Reducing sensitivity to the overall market

9:25 - Managed futures

15:40 - What indicators would change to become bullish?

22:35 - Tightening financial conditions

32:50 - Maxar Technologies

42:18 - Boxabl

Give this podcast a listen if you want to go deeper into our big picture and long term view.

Final Word- We are not a Hedge Fund

We are starting to get a lot of questions about the Fundamental Value Portfolio and if it is available as a separate private offering.

Tuttle Ventures is currently not a hedge fund.

We are a Registered Investment Advisor, and the portfolio is available to our advisory clients where we have trade discretion. We have the flexibility to charge performance based fees for qualified investors, which is outlined in our ADV.

We are not ruling out the option to convert into a private offering in the future, but at this time we have no immediate intention of changing fund operations.

As a client of Tuttle Ventures, rest assured that any considerations of the fund would be made to benefit you as our trusted partner first and foremost.

Thank you for reading and I am grateful and humbled to be able to learn, grow and invest alongside you at Tuttle Ventures.

Don’t forget to follow Tuttle Ventures on Twitter, LinkedIn or Instagram.

Check out the website or some other work here.

Best,

Darin Tuttle, CFA

NOTE - This is not investment advice. Do your own due diligence. I make no representation, warranty or undertaking, express or implied, as to the accuracy, reliability, completeness, or reasonableness of the information contained in this report. Any assumptions, opinions and estimates expressed in this report constitute my judgment as of the date thereof and is subject to change without notice. Any projections contained in the report are based on a number of assumptions as to market conditions. There is no guarantee that projected outcomes will be achieved. Unless there is a signed Investment Management or Financial Planning Agreement by both parties, Tuttle Ventures is not acting as your financial advisor or in any fiduciary capacity.