A look at Houlihan Lokey for the Fundamental Faithful

Deep Dive into an M&A Player from Tuttle Ventures

Welcome to +35 new subscribers this week & +416 over the last 90 days.

I am grateful and humbled to be able to learn, grow and invest alongside you at Tuttle Ventures.

Today is a post for the fundamental faithful.

We will send out portfolio updates and rationale tomorrow.

Catch last week’s update here.

The positive portfolio this quarter, during the challenging market, needs its own post to explain in detail why we are still short term bearish and how we are navigating the current macro environment.

It our goal to keep “dancing through the raindrops” towards the end of the year.

We get it, hot macro takes are not for everyone.

It’s been nearly 2 month since we wrote Mi Vida: Uranium Investing and gave an in-depth analysis of the fundamental drivers behind LEU 0.00%↑.

Readers following along got a chance to go on quite a ride in the uranium sector.

After the initial stock price of $42.43 on posting day, the stock price ran straight up for the next three weeks to a 52-week high of $54.61, only to slide back down to $40.61 as of Friday’s close.

At the time of this writing, we have no position in the stock.

A good old fashioned bottom up analysis is due

We interrupt our regular scheduled programing to give you our latest deep dive and bottom up fundamental research on HLI 0.00%↑ Houlihan Lokey, the global investment bank based in Los Angeles, California.

All charts from today’s post are kindly supported by Ycharts.

Our brilliant equity research associate Brandon La Bella, has been quite obsessed with M&A activity for the last several months.

As a reminder to readers, we look at all company financials as a crime scene— hiding management’s secrets.

We simply follow wherever the clues take us.

Access to our company excel model will be available to all paying subscribers.

A balanced fundamental take on Houlihan Lokey is especially difficult given the company is literally run by corporate financiers.

I mean these guys are smart and their books are going to of course look great. They do finance restructurings and M&A for their day-to-day job for heavens sake!

The Bottom Line First:

Houlihan Lokey (HLI) is a good business with strong management. The company should do OK through a potential recession with robust business revenues and strong cash position across corporate finance, restructuring, and M&A advisory business lines targeted at mid-market companies.

If you are currently holding the stock, we recommend holding and collecting the newly issued dividend.

If you are looking to buy, we think you will be able to buy at a lower bargain price over the next few months.

IBank and advisors are down 28% on average YTD (vs. the S&P 500 down 25%)

Fundamental Breakdown

Highlights have been added for emphasis.

Three things stand out:

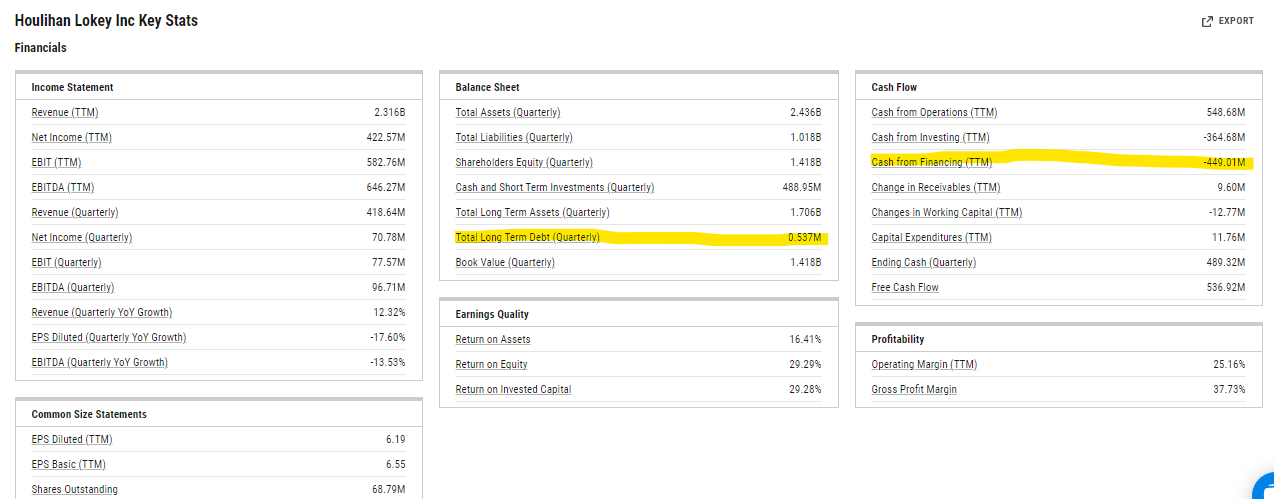

No debt on the Balance Sheet

Goodwill Gangster

Dressing up for an Acquisition Ball?

No Debt on the Balance Sheet

The first thing that immediately stands out is the lack of long-term debt on the balance sheet.

No debt is a red flag because it means the company does not have an existing banking relationship to fund growth over the next 5, 10 years. It appears they have not taken on any new debt over the course of several years which is well below industry competitors.

We call this the classic “Smith & Wesson Problem”. (From our past lessons learned investing in Smith & Wesson)

The essence of this problem comes down to this:

How do you fund future growth without taking advantage of the lowest interest rates in history?

It appears the company is self-financing growth.

Self financing for strong operators like this is usually an advantage because it gives management the ability to leverage internal assets themselves.

You can see this with -$449M in Cash from Financing TTM, mostly from changes in working capital by spending down current assets (Cash).

Here’s the other issue: When you self-finance growth, it means you need management to outperform on a consistent basis.

This can be a high bar for management to overcome, especially heading into a potential recession.

Any slip in revenues or cash flow can immediately stun future growth and cancel growth projects.

It also looks like they have been self financing by:

Increasing the number of outstanding shares (bad for shareholders)

Being more conservative in share buybacks, based on the March earnings statements (Bad for shareholders). 1.25M shares were bought at $103.80 in 3/31/22, that’s a paper loss of $35M QoQ. (Ouch!)

Goodwill Gangster

I define Goodwill as what you overpay to buy another company.

The $591M acquisition of Japan’s GCA was completed late last year, in two successive deals and the two firms have been operating together under the Houlihan Lokey brand in Europe and the United States since December 2021.

Nearly half, 43% of the company’s assets, are now tied up in Goodwill.

Nothing gets me more nervous than the potential for a write down or impairment on a huge acquisition.

Economic recessions historically lead to an increase in goodwill impairments. U.S. public firms took $143 billion in impairments in 2020, the most in at least a decade, according to Duff & Phelps.

HLI's restructuring revenues declined 35% QoQ (HLI is the only independent advisor to report restructuring separately), and came in 13% below consensus street estimates.

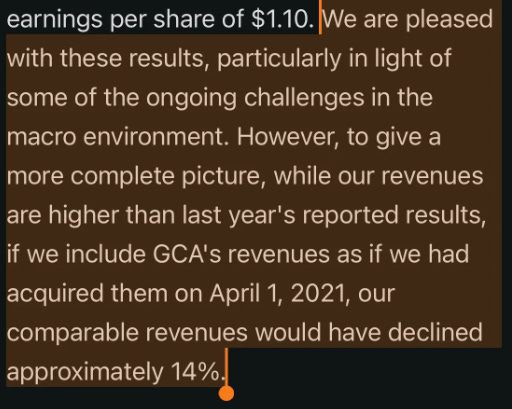

A closer look is needed at their most recent acquisition of GCA to see what is holding the company back.

From the most recent earnings call, the acquisition has not been keeping pace at the same levels of revenue growth on a YoY basis.

Nothing annoys me more when management backs out financials of a recent acquisition.

You bought the company, now its time to make your bed and sleep in it.

Is it possible a company that specializes in M&A deals bought a loser last year?

Not likely.

In the past, prior acquisitions have lead to revenue growth. See the purple line of revenue trending typically above the orange line of goodwill.

My personal take here is it just may require more time to for revenues to catch up over the next several quarters, but it’s something to keep an eye on.

Dressing up for an Acquisition Ball?

It appears management maybe setting the company up for a potential acquisition themselves.

This would explain no debt, new dividends, good operating performance, and cash on hand.

We believe, much like Japan of the early 1990’s, the bursting of bubbles has deep and wide-ranging second order effects, including the basic mind-set of investors of: “no more excess”.

Eventually we may get there and when we do, many of these failing publicly traded companies will become unsustainable, and a wave of consolidation could very likely take place.

Until then, based on research from Goldman Sachs and Deal logic M&A activity will slug along at a much slower pace.

The market appears to be discounting some probability of a recession and we believe this is in line with our broader view.

We have no position in the stock. Tuttle Ventures, acting as a fiduciary for investment clients may decide to make an initial investment within the next 48 hours based on clients individual risk tolerance and preferences.

Final Word

Thank you for reading and I am grateful and humbled to be able to learn, grow and invest alongside you at Tuttle Ventures.

Vision, Courage and Patience leads to successful investing.

Don’t forget to follow Tuttle Ventures on Twitter, LinkedIn or Instagram.

Check out the website or some other work here.

Best,

Darin Tuttle, CFA

NOTE - This is not investment advice. Do your own due diligence. I make no representation, warranty or undertaking, express or implied, as to the accuracy, reliability, completeness, or reasonableness of the information contained in this report. Any assumptions, opinions and estimates expressed in this report constitute my judgment as of the date thereof and is subject to change without notice. Any projections contained in the report are based on a number of assumptions as to market conditions. There is no guarantee that projected outcomes will be achieved. Unless there is a signed Investment Management or Financial Planning Agreement by both parties, Tuttle Ventures is not acting as your financial advisor or in any fiduciary capacity.

Houlihan Lokey and goodwill wow bad call financial sectors still going to get battered in a lot of economic gooey-ness. Plus, if you rewind the tape corporate ethics is really going to be something that is major these guys as corporate finance seers are almost leading to your initial gut reaction that they’re just gonna manipulate earnings up and down the block for corporations.