What to Expect when you're Expecting?

Actionable Market Insights from Tuttle Ventures

Welcome to +247 new subscribers over the last 90 days.

Catch me on live TV tomorrow, Monday at 9:45am ET on TD Ameritrade Network.

Newsletter rundown:

Short Term Inflation Expectations

What does the current market expect for inflation over the next 12 months?

What’s the best measure for inflation expectations in the short term?

ICE’s new measure for inflation expectations

Final Word

It seems like everyone has forgot about inflation.

Out of sight, out of mind.

I guess that’s what happens when investors are faced with a problem that hasn’t been around for 40 years.

The US personal savings rate—at 4%— is a historic low, falling below the rate of inflation.

The difference between savings and inflation is the most negative since 1960.

When people spend at a higher rate than they save (or invest) —higher prices tend to follow.

Bond markets are pricing in rate cuts in 2023, reflecting the old recession playbook where central banks cut rates on signs of economic and financial damages.

Yet persistent inflation means we expect rates to stay higher for longer.

What does the current market expect for inflation over the next 12 months?

The market expects inflation to come down, fast.

How fast?

That depends on what you’re looking at.

In my opinion, the market does a terrible job of pricing inflation expectations in the short term.

That’s why we believe there’s a 60% chance that inflation actually remains higher than market expectations over the next 12 months.

Let me explain:

Remember we are talking about expectations, not reality.

5 to 10 years out, we have a pretty good measure with Treasury Breakeven Rates.

This measure of expected inflation is calculated using measured yield differentials between nominal and inflation-protected Treasury securities (TIPs) at 10- and 5-year maturities.

Pretty much everyone looks at 5-year Treasury Breakeven Rates to infer inflation expectations… but what about expectations over the next 12 months?

That is not as clear cut.

Recent changes in markets and the economy have offset the capacity to accurately capture expectations.

We believe expectations matter when the yield curve is inverted because short term rates lead the flow of investment funding…

At a 6% inflation rate, it only takes 12 years for your initial investment value to be cut in half.

For the relative impact that inflation plays on investor returns, I think its worth asking, what’s the best measure for inflation expectations in the short term?

What’s the best measure for inflation expectations in the short term?

The standard proxies for inflation expectations are:

Survey of Consumer Expectations (NY Fed)

US Treasury Market (JP Morgan)

SOFR Swap Curve [annual/annual] (Chatham Financial)

Oil Spot Prices (West Texas Intermediate)

Everyone has a favorite, but none of them are any good.

Our research shows that:

People tend to lie in online surveys, correlations in the treasury market fall under high volatility regimes, Swap rates don’t always reflect executable levels and oil spot prices are at the whim of OPEC and geopolitical tensions.

Add in the transition of $200 trillion of financial contracts referencing USD LIBOR and you really start to see why no one saw inflation coming from traditional proxies.

That’s where ICE’s new measure for inflation expectations comes in…

ICE’s new measure for inflation expectations

In September 2022, the Intercontinental Exchange, Inc. (ICE) introduced the ICE U.S. Dollar Inflation Expectations Index Family to help investors gauge future inflation expectations and inform policy and risk management decision making.

The index is based on trading in Treasury Inflation Protected Securities (TIPS) and inflation swaps contracts.

Currently the index is free because it is still in the testing phase.

The weighting of TIPS vs Swap derived prices in the calculation of the CPI projection is determined based on estimates of trading activity. The ratio was initially set at 3:1 (weighting of TIPS and treasury prices is three times greater than inflation swaps prices).

The index goes further to calculate the implied market inflation expectations by sourcing price/yield data from the U.S. Treasury Inflation Protected Securities (TIPS), Treasury Bills, Notes and Bonds, and the inflation linked swaps markets.

By combining both Treasury market data (TIPS real yields relative to like maturity nominal Bill, Notes and Bonds yields) with inflation swaps pricing data, the index sources input from the two deepest and most liquid inflation-linked markets to build the index settings.

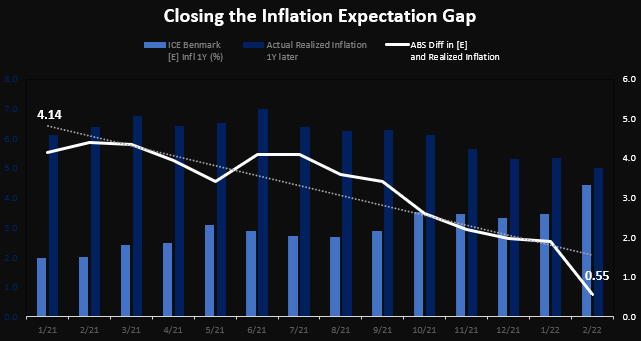

To examine the index, we looked at its relative predictability on a 1-year basis.

As expected as of January of 2021, more than two years ago, expectations were way off.

However, as inflation has become part of the market narrative, the difference between expectations and reality has significantly narrowed— from 4.14 to 0.55 bps over the course of 13 months. (see chart above)

This demonstrates that short term expectations of the index have improved in accuracy.

Expectations also suggest that peak inflation expectations were “priced in” for this month of 3/2023 at a rate of 5.32%.

What we think is meaningful is the steady consistent downtrend from here, with expectations on a decline to 2.60%.

A current one year market expectation of inflation at 2.60% tells me two things.

First, the market sees stubbornly high inflation keeping the Fed from reaching their 2.00% target before the end of 2023.

Second, the new information from SVB has failed to update inflation expectations.

Despite all the hardline talk, the market hasn’t shaken the fact that inflation is here to stay, above its target.

We think this increases the probability of more upside surprises to inflation.

Stubbornly high inflation is really driven by services.

Goods prices have fallen, dragging overall inflation down but wage growth has persisted and is fueling stickier core services inflation.

This is something we will continue to watch going forward.

Final Word

We are overweight equities in our strategic view with a tilt towards energy and value.

We estimate the overall return of stocks will be greater than fixed-income assets over the coming decade.

Tactically, we’re underweight technology stocks as we believe central banks’ rate hikes cause financial cracks and economic damage to the ill prepared.

Corporate earnings expectations have yet to fully reflect even a modest recession and inflation expectations are overly optimistic.

If you’d like to set up time to discuss your portfolio, please schedule a time below:

Meetings with Darin Tuttle

Best regards,

This is not investment advice. Do your own due diligence. I make no representation, warranty or undertaking, express or implied, as to the accuracy, reliability, completeness, or reasonableness of the information contained in this report. Any assumptions, opinions and estimates expressed in this report constitute my judgment as of the date thereof and is subject to change without notice. Any projections contained in the report are based on a number of assumptions as to market conditions. There is no guarantee that projected outcomes will be achieved.

Neither the publisher nor any of its affiliates accepts any liability whatsoever for any direct or consequential loss howsoever arising, directly or indirectly, from any use of the information contained herein.

Unless there is a signed Investment Management or Financial Planning Agreement by both parties, Tuttle Ventures is not acting as your financial advisor or in any fiduciary capacity.

Clever title! I like it!

Good inflation info! 👍

Nasdaq is looking pretty bullish... I'm a tech guy but am hedging. I think equities are looking a little too rosy out of the gate YTD.