Special Event: Depeg Discount

Actionable market Insights from Darin Tuttle

As my readers know, I’m no market timer, I’m a value investor.

I was working on an update to the second half of the 2023 investing playbook when I stumbled upon a unique value trading opportunity.

Summary

NGE 0.00%↑ Global X MSCI Nigeria ETF invests in the largest and most highly-traded companies in Nigeria.

The Fund is up +25% this month on the news that the ETF is going to be closed and liquidated.

The Fund will cease trading at the end of the trading day on July 28th, 2023.

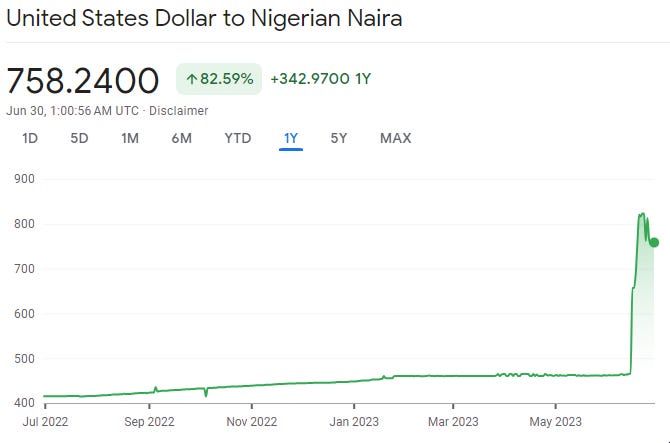

The decision to close the Fund came after the Nigerian government dropped the currency peg of the Naira/USD on June 14th. The uncertainty surrounding future foreign exchange policy as a de-pegged currency remains high.

Based on the prospectus, Global X is still on the hook for the liquidation of the Fund to be settled in USD. This is why there is a distinct opportunity over the next 30 days while there is still a discount to NAV.

We expect ~11% upside and favorable risk/reward in buying the ETF at a low market price and holding over the next month as the Fund converges to NAV.

Shares of ETFs are bought and sold at market price (not NAV) and are not individually redeemed from the Fund. Brokerage commissions will reduce returns. The liquidation of the Fund will be a taxable event for investors.

Carefully consider the fund's investment objectives, risks, and charges and expenses before investing. This and other information can be found in the fund's full or summary prospectuses, which may be obtained at globalxetfs.com. Please read the prospectus carefully before investing.

Why Now?

In emerging market economies, historic events can happen fast.

After the election of the new president Bola Tinubu on 29 May, the Nigerian Central Bank made a surprise move to remove the USD peg on their local currency.

The economic development of Nigeria has been significantly hindered by military rule, mismanagement, corruption and ethnic conflict.

The Nigerian economy is heavily dependent on oil production and sales and prices of oil in global markets, and the industry makes up a significant portion of Nigeria’s GDP.

Nigeria has long suffered FX shortages, oppressive energy prices, and runaway inflation because of a reliance on the US Dollar.

The annual inflation rate in Nigeria rose for the fourth month to a near 18-year high of 22.41% in May 2023

Every country has its breaking point.

This could be a step in the right direction.

According to the World Bank:

Nigeria could save up to 3.9 trillion naira ($5.10 billion) this year alone after reforms to its foreign exchange market and the removal of the petrol subsidy.

This is all part of a broader theme of self interested sovereign African nations that are working for their own best interest and not playing to US empirical rule.

Since the de-peg, the exchange rate has exploded and the US Dollar has strengthened by 82% relative to the Nigerian Naira.

This has been the largest currency depreciations this year.

That being said, research coming out of Goldman Sachs believes that the sharp devaluation may be emotionally overblown, with the chance of a slight strengthening of the Naira relative to the USD as the sting of the de-peg dissipates over the coming months.

Our research supports that view.

The US is still looking to cooperate with Nigeria and the newly elected president.

In fact, the US State Department on June 26th announced a visit to Nigeria by Assistant Secretary for Energy Resources Geoffrey R. Pyatt, and the formation of an Energy Security Dialogue with Nigeria to advance collaboration on our shared energy and climate goals.

We see this as a step in the right direction for both countries.

Without going too deep into the macro picture, (too late?) the key point here is to recognize the economic incentives Bola had to make such a drastic move and cooperative position of the US economic interests.

The Discount

Shifting gears, its important to focus on the discount to the NAV which creates a narrow window before the closing of the Fund.

ETFs rarely stray far from their underlying net asset values because it is usually the job of The New York Stock Exchange, Global X as ETF issuer, and GTS as the Lead Market Maker to ensure market prices trade close to their true intrinsic value.

The NAV discount for NGE 0.00%↑ stands out because it is a security that is traded throughout the day and still a large discount, almost reaching as high as 50% a few days ago…

Closing this discount has historically been a challenge because Nigeria has long suffered FX shortages on both sides (Dollars and Naira).

There are also no options to trade the ETF…

The current NAV is $11.23 as of 6/28/2023, while the ETF is trading in the market at $10.05.

You could naively calculate $11.23 -$10.05= $1.18/share as a potential premium.

That is nearly 10.5% (1.18 divided by 11.23) or $3.5M in potential value spread based on $33.5M in total AUM (Assets Under Management) of the Fund.

In my opinion, this gap in value is relatively too small for larger institutional players to participate in.

According to the NYSE Exchange rules, Shareholders may sell their holdings in the Fund prior to the close of regular trading on the Closing Date and customary brokerage charges may apply to these transactions.

Key Risks

Prior to the closing date, Global X will be in the process of winding up its operations in an orderly fashion and liquidating its portfolio.

A key risk to mention, although a low probability, is that the NYSE steps in and overrules Global X’s liquidation process.

NYSE Arca has the authority to adopt a revised selection policy for issuers in the event of unusual circumstances.

We would say that this could be one of those unusual circumstances.

Despite this risk, we think the exchange will allow the market to function regularly. ‘

In 2021, there were 120 closed (liquidated or merged) ETFs, so this is a common enough occurrence.

Another risk is tracking error. Tracking error is the divergence between the price behavior of the Fund and the price behavior of the benchmark. The selling of the Nigerian stock holdings may result in the Fund not tracking its underlying index. This makes it difficult to properly manage risk.

To increase its USD cash holdings, performance may not be consistent with the Fund’s current investment objective and strategy because they will be forced to sell.

In a typical arbitrage opportunity, a fund manager would want to go both long and short to balance each side of the trade, reducing directional market risk.

In this scenario, it would mean going long the ETF and shorting the underlying stock holdings.

Because of the disconnect to the underlying benchmark, we view shorting the underlying as a greater risk than necessary.

We cannot guarantee shorting the Nigeria stocks will be able to offer a full hedge in the short timeframe.

There is also the risk that Global X does not have the funds to pay.

Global X as the advisor will bear all fees and expenses that may be incurred in connection with the liquidation of the Fund and the distribution of cash proceeds to investors in the Fund, other than brokerage fees and expenses.

However, we believe that Global X, who has more than 100 ETF strategies and over $40 billion in assets under management, will to honor the ~$35M in USD to payout to shareholders.

Not paying out on this ETF may scare investors in other funds and damage the brand reputation.

Final Word

Despite these risks, and others we did not mention or may have missed, we are positive about the opportunity.

On or about August 1, 2023, the Fund will liquidate its assets and distribute cash pro rata to all remaining shareholders who have not previously redeemed their shares in an amount equal to the net asset value of their shares as of the close of business on that date.

These distributions will be taxable events.

In addition, these payments to shareholders will include accrued capital gains and dividends, if any.

I am grateful and humbled to be able to learn, grow and invest alongside you at Tuttle Ventures.

Vision, Courage, and Patience leads to successful investing.

Best,

Darin Tuttle, CFA

I/we may take a beneficial long position in the shares of NGE 0.00%↑ either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I have no business relationship with any company whose stock is mentioned in this article.

This is not investment advice. Do your own due diligence. I make no representation, warranty or undertaking, express or implied, as to the accuracy, reliability, completeness, or reasonableness of the information contained in this report. Any assumptions, opinions and estimates expressed in this report constitute my judgment as of the date thereof and is subject to change without notice. Any projections contained in the report are based on a number of assumptions as to market conditions. There is no guarantee that projected outcomes will be achieved.

Neither the publisher nor any of its affiliates accepts any liability whatsoever for any direct or consequential loss howsoever arising, directly or indirectly, from any use of the information contained herein.

Unless there is a signed Investment Management or Financial Planning Agreement by both parties, Tuttle Ventures is not acting as your financial advisor or in any fiduciary capacity.

Nice! I have owned NGE as a diversifier. The risk: reward on the arb play is interesting.