Decoding the CME FedWatch Tool: Navigating the Realities of Short-Term Interest Rate Bets

Beyond Market Noise: A Practical Look at the Real Impact of Rate Predictions on Long-Term Investments

Everyone loves quoting the CME FedWatch Tool, but most don't understand what the cost of being "wrong" on a relatively trivial 8 day hedge is.

Let me share a secret with you, its not much.

If you're unaware of the costs of incorrect predictions and don't trade 30-day Fed Fund futures, this measure is irrelevant for long-term asset allocation.

Let me show you an example and then outline what you should be focusing on to maximize the value of your investments.

Imagine I had $10,000,000 and I bet the new rate will be 5.00% instead of 5.25% the cost is only $549.49 in lost interest.

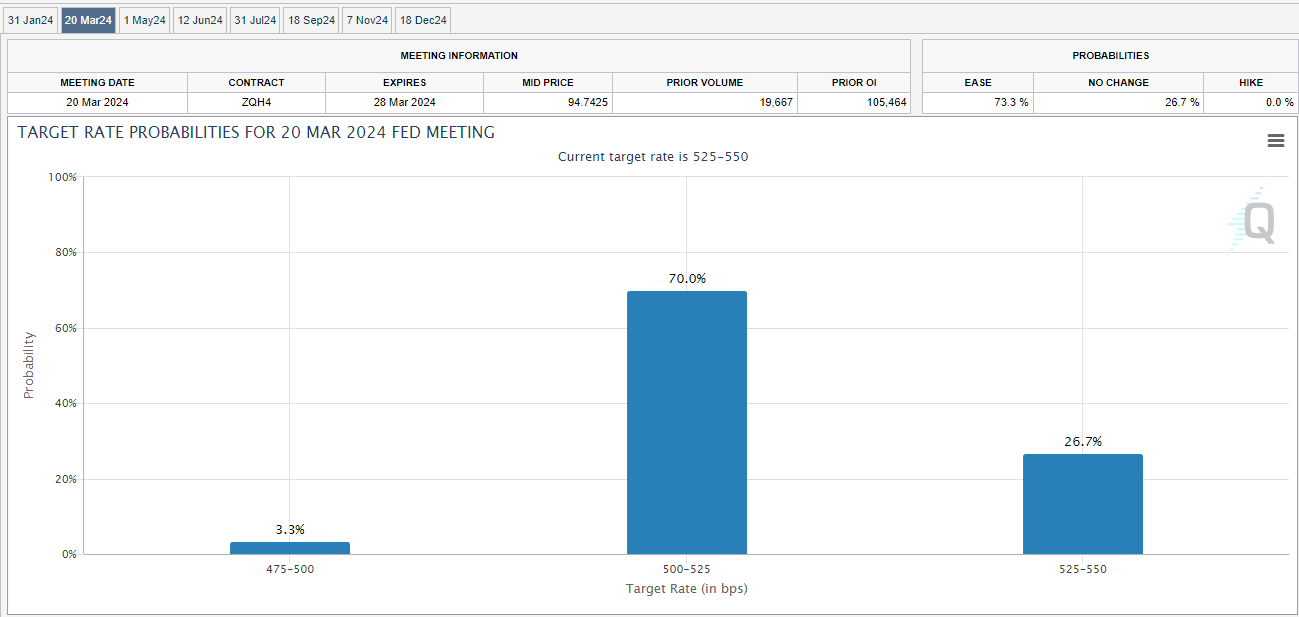

The chart above showing a 70% chance of a rate cut is using the ZQH4 futures contract.

The difference between when the Fed could potentially cut during the March 20th meeting and the March 28th futures contract expiry is only 8 days difference and a total 73 days from today.

If I am able to earn 5.25%, or a daily rate of 0.014383% with overnight reverse repo, I could end up with $10,105,541 at the end of the 73 days.

Future Value for the Full 73 Days at 5.25%: Daily compounding (N=73, I/Y= 0.014383, PV= 10,000,000, PMT= 0, FV= 10,105,541)

In a revised scenario, and the Fed decides to cut by 0.25%, you earn an annualized rate of 5.25% for the first 65 days and then 5.00% for the remaining 8 days, the calculations would look like this:

Future Value for the First 65 Days at 5.25%: The future value of your $10,000,000 investment after 65 days at an annualized rate of 5.25% would be approximately $10,093,924.

Future Value for the Last 8 Days at 5.00%: Using the future value from the first period as the principal for the last 8 days, the future value after these 8 days at an annualized rate of 5.00% would be approximately $10,104,991.

Cost of Being Wrong in This Scenario:

The difference between the future value calculated at a constant 5.25% rate for the entire 73 days ($10,105,541) and the future value in this new scenario is approximately $549.49.

This represents the lost interest due to the lower rate in the last part of the period compared to maintaining the higher rate throughout the entire period.

But here’s the problem, you are only locking in a higher rate for 8 days.

When the cost of being wrong is small, its just market noise.

The probabilities of the March contract are just noise.

So what does matter?

Investors should be asking themselves “What are the chances of locking in higher rates for longer periods of time?”

Rate cut probabilities later in the year are more significant, as the cost of miscalculation is higher.