2023 Investing Playbook: Bonds are Back

Why 2023 will be Fixed Income’s time to shine

*This is sponsored advertising content and the disclaimer at the bottom of this email must be read carefully.

Finny sends you free personal finance insights so you can make better money moves

When it comes down to learning good money habits, there's so much jargon out there. Finny's newsletter, The Gist, is different. Twice a week, you'll get simple 5-minute breakdowns of top money trends, personal finance, and investing tips delivered right to your inbox - for free. We highly recommend it.

2023 Investing Playbook

Today we are sending out our 2023 Investing Playbook.

Bottom Line: We think 2023 will be a year to rethink fixed income as an attractive risk/return opportunity for actively managed portfolios.

We see a compelling case for bonds. Alongside what we see as attractive yield potential, fixed income also looks favorable from a macroeconomic perspective – bonds historically tend to be resilient in a recession.

Long time readers know this is a complete 180° turnaround from what I’ve said for years.

As the fundamental investor, bond math has now shifted on expected inflation, interest rates and credit risk.

The asset class looks materially different from back in January of this year when I wrote 2 Questions for 2022.

Let’s dive in.

Playbook Lineup:

Why Bond Math Looks Good

Risk‑Off, Yield‑On: Emerging Market Debt in Focus

Countries at the top of our list: Current cross-asset signals favor Emerging Market Debt in Mexico, Korea and Brazil. (In that order)

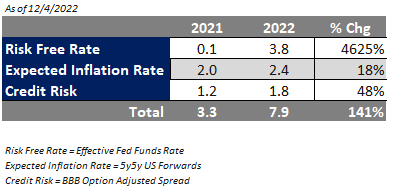

Why Bond Math Looks Good

When I say “Bond Math Looks Good” remember that bond yields are simply a combination of Risk-Free Rates, Expected Inflation Rates, Credit Risk, and other risk premiums.

Look how far we have come comparing 2021 to 2022:

The repricing in the bond market has been nothing short of extraordinary in 2022.

We believe the market has done enough and sufficiently repriced bonds at attractive levels across most possible scenarios for 2023.

Higher yields are a gift to investors who have long been starved for income at the lowest risk premiums in decades. At 4.25% yields or greater, short-term government bonds, emerging market debt and mortgage securities are appealing.

We plan to stage in and buy fixed income securities throughout 2023.

We are staging because the upside potential needs to be weighed carefully against the capital loss associated with a more rapid increase in rates. The terminal rate is still in question at this point.

CPI YoY% in 2023 is going to plummet.

Remember CPI is a % comparison to the prior year. We are now going to be comparing against incredibly high levels.

The last four CPI prints have averaged +0.23%. If monthly inflation increases by 0.30% in 2023, we'll be at 3% YoY inflation June 2023.

0.3 x 12 = 3.6

Bond Math Looks good.

Risk‑Off, Yield‑On: Emerging Market Debt in Focus

Over the past two decades, the EM debt market has grown significantly.

Based on State Streets estimates, this universe of index-eligible securities stood at about US$7.3 trillion at the end of December 2021.

We think this makes it too big a market for global investors to ignore.

Emerging Market Debt is a "risk on" trade that perform particularly well during periods of middling growth and declining global interest rates.

According to Morgan Stanley Research, Emerging Market (EM) debt could benefit from a combination of trends—including declining rates, improving economic fundamentals and a weakening dollar.

Fixed-income strategists forecast a 14.1% total return for emerging market credit, driven by a 5% excess return and a 9.1% contribution from falling U.S. Treasury yield. Emerging market local currency denominated debt should see an even stronger total return of 18.3%.

EM debt has led EM equities by 170bps per yr. for the past 30 years.

As of June 30, the J.P. Morgan Emerging Markets Global Bond Index Diversified yield stood at 8.57%. For comparison, this yield just touched 8% during the peak of the COVID liquidity crisis in March of 2020, and the last time we saw these levels was in the aftermath of the global financial crisis.

For fixed income investors willing to move out on the risk spectrum, Emerging Market Debt presents a significant yield pick-up opportunity.

As of 12/4/2022 The 30 day SEC yield for VWOB 0.00%↑ Vanguard Emerging Markets Government Bond ETF is 6.89%.

Emerging markets debt is further along in its adjustment than even the initial Bond Math I laid out earlier.

This is all because of King US Dollar.

Emerging markets currencies have exhibited remarkable resilience compared with developed markets currencies such as the yen and euro. Thus far in 2022, emerging markets currencies are down around 10% versus the dollar, while developed markets currencies are down around 18% against the US currency. This relative strength is likely due to several factors, including aggressive and proactive central bank rate hikes in emerging markets, already cheap valuations, and light investor positioning as a result of significant fund outflows.

A quick formula to remember for all investors: Fed pivot = dollar weakness

Triggered by early signs of global monetary tightening, the emerging markets sell-off began in the fourth quarter of 2021, much earlier than in the sell-off in the broader credit market.

That's one reason we believe emerging markets debt is closer to its bottom and better positioned for recovery than other asset classes. The rapid selloff in spreads and global interest rates has resulted in historically low dollar prices for emerging markets bonds.

According to Goldman Sachs Investment Research, sovereign credit has historically proved to be the most defensive during the last part of the business cycle, where growth rates are still dropping but central banks have changed tack and the market is pricing cuts.

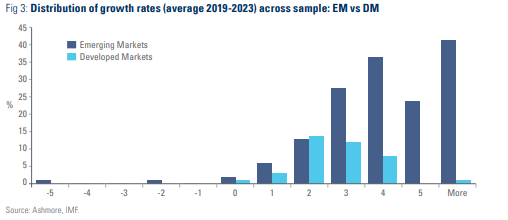

Another reason to be bullish is relative growth rates to Developed Markets.

If you haven’t noticed lately Developed Markets have sure been acting a lot like Emerging Markets.

However, when you compare the distribution of growth rates EMs are still relatively attractive.

Exposures linked to carry, defensive, momentum and valuation themes have been well compensated in EM markets and researched by AQR.

While it's always hard to pick the exact bottom, we feel comfortable about the outlook for emerging market debt.

Countries at the top of our list: Mexico, Korea, Brazil

We like the set up for Mexico, Korea and Brazil. In this post, I’ll concentrate on Mexico specifically.

We believe the sovereign debt of an emerging market country is ultimately tied to its future growth prospects and ability to tax future growth.

Total tax revenue as a percentage of GDP indicates the share of a country's output that is collected by the government through taxes.

Between 1965 and 2020, the average tax-to-GDP ratio in the OECD area increased from 24.9% to 33.6%, an increase of 8.7 percentage points.

Mexico has the lowest tax-to-GDP ratio (16.7%).

Mexico has both the ability and capacity to tax future growth.

Mexico is also the second-largest local bond market, after Brazil, in Latin America.

In 2023, we believe Mexico will benefit from increased industrial production. While the US pretends to be the recipient of shifting supply chains, Mexico is in a much better position.

The manufacturing lines are almost off the charts:

This shift in manufacturing would allow Mexico to clearly take advantage of the opportunities provided by the reconfiguration of global value chains to attract productive investment with greater added value.

Government debt of about 60 percent of GDP is not considered a problem.

The government can make payments without strain and even has some room to borrow more. If debt levels reach 80-90 percent that may have negative effects on the economy. Debt above 120 percent of GDP is quite detrimental.

When the pace of economic growth exceeds the rate of interest on a country’s debt, managing indebtedness becomes substantially easier.

Foreign investors are the single largest holder of domestic debt market securities (owning 25% of the outstanding amount as of January 2015, according to Banxico), and foreign investors have been an important marginal price setter.

Domestic institutional investors, led by pension funds, also provide strong support for local bonds.

Pension funds currently own around 50% of long-end government bonds.

All of this depends of course on a weaking US Dollar.

US Dollar to Mexican Peso Exchange Rate is at a current level of 19.27, down from 19.29 the previous market day and down from 21.29 one year ago.

We expect this trend to continue.

Final Word

Thank you for reading and I am grateful and humbled to be able to learn, grow and invest alongside you at Tuttle Ventures. Vision, Courage and Patience leads to successful investing.

Don’t forget to follow Tuttle Ventures on Twitter, LinkedIn or Instagram.

Check out the website or some other work here.

Best,

Darin Tuttle, CFA

NOTE - Advertising helps us keep the lights on — and continue offering the content you love, for free. Sponsored content may pay the Tuttle Ventures Newsletter a credit if you click through an application linked on the site. This allows us to maintain the time to perform editorial work and bring together the newsletter you know and trust.

This is not investment advice. Do your own due diligence. I make no representation, warranty or undertaking, express or implied, as to the accuracy, reliability, completeness, or reasonableness of the information contained in this report. Any assumptions, opinions and estimates expressed in this report constitute my judgment as of the date thereof and is subject to change without notice. Any projections contained in the report are based on a number of assumptions as to market conditions. There is no guarantee that projected outcomes will be achieved.

Neither the publisher nor any of its affiliates accepts any liability whatsoever for any direct or consequential loss howsoever arising, directly or indirectly, from any use of the information contained herein.

Unless there is a signed Investment Management or Financial Planning Agreement by both parties, Tuttle Ventures is not acting as your financial advisor or in any fiduciary capacity.

Great newsletter!